The mental gymnastics of manufactured austerity

Why the UK’s obsession with 'balancing the books' is the only thing standing between it and a thriving economy.

A version of this article was published in The New Statesman on 7 December 2025.

During my first experience working in UK local government with the London Borough of Hackney’s homelessness prevention service, I remember being asked by a senior manager: ‘Have you ever worked in a system this insane before?’ I assumed she was referring to the thousands of families living in temporary accommodation, the housing officers overburdened with ever-expanding case loads and the utter lack of resources to really do much of anything about it.

I pondered for a second and replied, ‘Yes, I have actually’. The local authority dilemma of trying to do more with less while serving vulnerable populations reminded me of my time working for an under-resourced school back home in Indianapolis - overcrowded classrooms, special needs case loads double the size of statutory limits and teachers burnt out by the outsized pressure to deliver impossible results.

Like the US education system, UK local government has been severely underfunded for years. The National Audit Office reported that government-funded spending power for local authorities decreased by more than 50% between 2010 and 2021. Since 2018, four times as many local authorities have gone bankrupt than in the past 30 years combined. It’s no surprise that the debt pile for all UK councils currently sits at £122 billion.

Although Conservative-led governments oversaw this managed decline of public services, Labour - a party traditionally in favour of public investment - has struggled to escape austerity’s grasp. Despite providing local authorities with a short-term funding boost in 2024/25, spending on unprotected services (e.g. social care, libraries and criminal justice) is still expected to decline in real terms by 1.3% per year after 2025/26. Labour has also attempted to reduce benefits like the winter fuel allowance and support for those with disabilities.

Labour’s ‘tough choices’ have led Anoosh Chakelian to argue that “Britain is trapped in Forever Austerity”. A 4% increase to NHS funding doesn’t matter much if the lack of social care drives up health inequalities. Nor does £39bn for new homes if council planning departments don’t have the capacity to deliver those homes at pace.

Herein lies the issue — even a political party elected on the promise of delivering change is trapped in the same outdated thinking that has held the UK back from realising its full potential. It’s becoming increasingly difficult to justify a brand of economics that disproportionately impacts those most in need while subjecting public servants — people who genuinely want to help — to a scarcity mindset they can never quite escape.

Austerity is a political choice, not an economic necessity. The reason political parties across the spectrum continue to fall into the same trap is because the entire way we think about government finances is deeply flawed. The idea that the government must cut services or raise taxes to fund public investment simply does not apply to a country like the UK.

Understanding this reality could be the shift that finally sets Britain free and positions it to deliver the thriving future its people so desperately need.

Why government finances don’t work the way we think

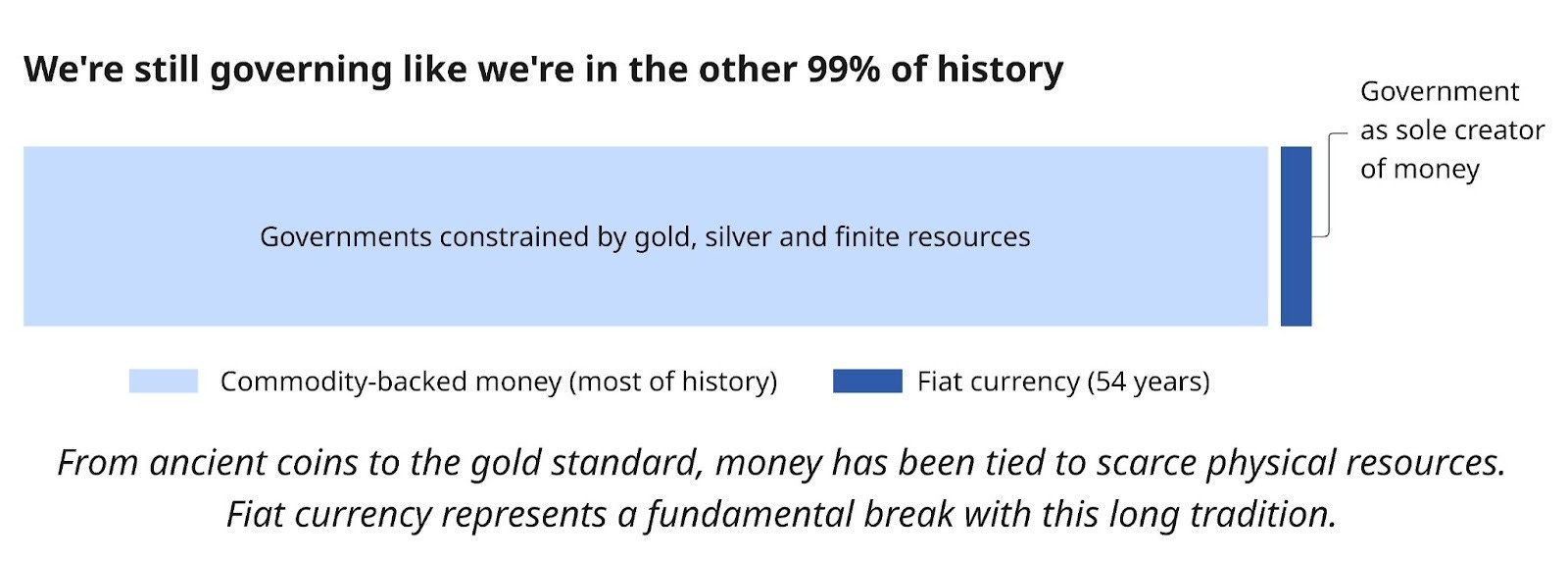

Although we must still hold leaders accountable for the current failures, it’s important to acknowledge that for most of history government finances have worked in a way that made austerity a rational policy choice (albeit a painful one). Under monetary systems like the gold standard, accruing debt meant depleting finite gold reserves, putting the government at risk of insolvency and economic collapse. When debt levels would rise too high, austerity was the obvious answer: cut government spending and raise taxes to bring the debt back down.

But when the US abandoned gold in 1971, everything changed. What started as a desperate measure to stop haemorrhaging gold reserves during the Vietnam War became a permanent feature of the global economic system. Attempts to restore the gold standard quickly failed as the number of dollars in circulation had outgrown the supply of gold, requiring either crippling deflation or forfeiting the dollar’s dominance in global trade. For the first time in modern history, money was no longer backed by a physical commodity but by government credibility alone.

Leaders at the time understood that the shift to what is referred to as fiat money gave them more flexibility during crises to run larger deficits when they needed to. But what many still don’t grasp to this day is that abandoning commodity-backed currency fundamentally transformed the way government finances work. Countries like the US and the UK suddenly became powerful currency issuers rather than mere users.

You and I, along with businesses, local authorities and most other actors in the economy are users of currency. We must earn or borrow money before we can spend. We need to balance the books and ideally generate a surplus so we can save for the future. Currency issuers on the other hand play by a different set of rules.

According to Richard Murphy, Professor Emeritus of Accounting Practice at the University of Sheffield, “A currency-issuing government cannot run out of money. It can always pay in its own currency”. Whereas governments historically needed to raise revenue through taxation or borrowing, this no longer applies to currency-issuing governments. In fact, economist Stephanie Kelton explains in The Deficit Myth that the sequence is reversed: currency issuers must spend first to put money into circulation before people can use that money to pay taxes or buy gilts. To paraphrase her, taxpayers don’t fund the government; the government funds the taxpayers.

This fundamentally changes the calculus of government finances. Most notably, currency-issuing governments don’t need to balance the books. Running deficits and accruing debt is not the solvency risk it once was. Alan Greenspan, the former Chair of The Federal Reserve said it himself: “The United States can pay any debt it has because we can always print money to do that. So there is zero probability of default.” The same is true for the UK. Similarly, taxes aren’t needed to raise revenue; they serve other purposes, such as managing inflation (taking money out of the economy), creating demand for the currency (we must pay our taxes in pounds sterling) and redistributing wealth.

This doesn’t mean there aren’t real constraints, however. While currency issuers don’t have to worry about the debt most of us fear, they do have to worry about demand-pull inflation, which occurs when there’s too much money relative to available goods and services. Carelessly creating new money without anywhere productive for that money to go runs the risk of crippling hyperinflation and economic instability. This is distinct from the cost-push inflation caused by external supply shocks, which is largely responsible for the UK’s recent price increases.

The primary limitation for currency issuers therefore is not the size of the public debt but the economy’s productive capacity — the ability to convert money into real goods and services. As Kelton explains, “Every economy has its own internal speed limit. It’s only possible to produce so much, at any point in time, given the real resources — people, factories, machines, raw materials - available in that moment.” Spend beyond what the economy can produce and you get inflation. Spend too little while resources sit idle and you condemn the economy to stagnation.

Modern Monetary Theory (MMT), the economic framework that explains this reality, is not so much a theory as it is an honest description of how government finances work in the fiat currency era. Bill Mitchell, Professor Emeritus of Economics at the University of Newcastle, Australia, says, “Such an understanding will change the questions we ask of our politicians and the range of acceptable answers that they will be able to give”.

This expands what’s politically possible. Rather than tying themselves in knots to balance the books, currency-issuing governments can properly steward the economy. With greater control over the money supply, they can more strategically deploy fiscal policy to mobilise idle resources (e.g. unemployed workers, crumbling infrastructure), fund transformative public investments and actually expand productive capacity in ways that were limited under the gold standard. The question is not whether we can afford a brighter future, but whether we have the resources to build it.

The issue is that we’re still governing like we’re in the other 99% of history, treating government finances like a household budget and subjecting everyone to artificial constraints that are no longer needed. When the US abandoned gold, the nature of money changed but our mental models didn’t.

This lag in up-to-date thinking has had devastating consequences for the UK economy. GDP is £11,000 less per person than if pre-2008 growth had continued. Infrastructure investment lags £700 bn behind what experts say is needed. And Britain is the only advanced economy where economic inactivity has increased since the pandemic. According to the Institute for Fiscal Studies, the UK’s productivity decline is largely due to the government choosing “not to [invest] due to the growing deficit”. The fact the UK’s debt-to-GDP ratio is approaching 100 per cent is not because the government overspent, but because austerity stifled the very growth needed to address it.

But the mental gymnastics persist. Although Reeves claims “there can be no return to austerity”, her fiscal rules of balancing the Budget and paying off the debt prevent her from leaving it behind for good. Despite welcome infrastructure investment, Reeves decided to freeze income tax thresholds for longer than expected, stealthily raising taxes for millions in the future. At the same time, the Resolution Foundation warns that public services outside of the NHS, education and defence will still face cuts toward the end of the decade close to those made during “peak austerity years”.

Meanwhile, the number of families living in temporary accommodation continues to reach record highs. What makes this failure even more damning is that the UK has complete monetary sovereignty: not only the ability to issue its own currency, but maintain a floating exchange rate, avoid borrowing in foreign currencies and have no external fiscal restrictions (foreign investors do own roughly 25 per cent of UK debt but that debt is denominated in pounds). This gives the UK a strategic advantage over its Eurozone neighbours.

Brexit: a blessing in disguise?

Despite keeping the pound sterling and opting out of punitive sanctions under the Maastricht Treaty, the UK was still subject to fiscal coordination requirements, such as limiting deficits to 3% of GDP and maintaining a debt-to-GDP ratio below 60% as an EU member. While the UK could have leveraged its exception to avoid austerity, doing so would have carried political consequences. Twice the European Commission opened an Excessive Deficit Procedure (EDP) against the UK, first from 2005-2007 and then again from 2008-2017 as it struggled to recover from the financial crisis. Both times, it complied with EU recommendations on how to correct its deficits.

Post-Brexit, although few seem to have noticed, the UK has stumbled into an ideal situation that puts it in an envious position over its eurozone neighbours. Not only are they bound by stricter fiscal rules than the UK ever was, but by adopting the euro they’ve been relegated to mere currency users. Unable to create their own money and dependent on the European Central Bank, they’ve forfeited their monetary sovereignty entirely. As Nobel-winning economist Joseph Stiglitz writes, “the eurozone was flawed at birth”.

This dysfunctional setup has had serious consequences for the region’s economies. France and Germany both have significant economic slack but struggle to deploy the fiscal expansion needed to mobilise it. Spain’s youth unemployment has exceeded 25% for years, yet eurozone rules limit the fiscal response needed to address it.

Most devastating has been Greece’s debt crisis. As a currency user, Greece faced genuine insolvency. The economy contracted by 25%, unemployment exceeded 27% and the country was forced into punishing austerity. Had Greece maintained its monetary sovereignty with the Drachma, it could have managed the crisis more effectively and prevented years of suffering. Yanis Varoufakis, the Greek economist who served as Finance Minister during the crisis, says: “We have created the gold standard in the middle of Europe. As we know, the gold standard is pretty good during the good times and it’s really appalling in bad times”.

By leaving the EU, the UK hasn’t just escaped cumbersome fiscal monitoring, it’s untangled itself politically from a group of currency users that don’t share its fiscal freedom. Nevertheless, the UK continues to squander this strategic advantage. Rather than binding rules like the EU, the UK’s fiscal targets are voluntary political commitments set by the Chancellor that can be changed at any time. Reeves for example decided on two self-imposed targets: day-to-day spending must be matched by tax revenues (i.e. a balanced budget) and debt must be falling as a share of GDP, both by fiscal year 2029/30.

In 2024, Reeves was barely within range to achieve a balanced budget by 2029/30. Ahead of the Autumn 2025 Budget, a projected 0.3 per cent downgrade in the Office for Budget Responsibility’s productivity forecast created a £20 bn shortfall that forced Reeves to consider raising the headline income tax rate for the first time since 1975. Even though last-minute projections ended up being more favourable than anticipated, this still demonstrates an obsession with satisfying arbitrary rules above all else.

To clarify, these policy decisions are not driven by actual economic events but by minor tweaks to imperfect OBR models about what might happen in the future. According to Larry Elliot, the longstanding economics editor at The Guardian, “The OBR struggles to forecast accurately what will happen to the public finances one year ahead, let alone four years ahead…the OBR’s forecasts are just guesswork. Informed guesswork, but still guesswork”.

Instead of using its monetary sovereignty to invest in ways that actually improve the fiscal picture long-term, the UK system, with its arbitrary rules and abstract modelling, favours the very austerity that makes low growth inevitable. While Brexit is routinely blamed by politicians, including Reeves herself, for the UK’s poor economic performance, leaving has gifted it the full monetary sovereignty that eurozone countries could only dream of. Regardless of whether it was the right decision, the real debate now is how the UK can leverage its fiscal freedom to finally build an economy that works.

Charting a new course

Recently, I facilitated a creative thinking exercise with GPs from the NHS where participants go through three rounds of making changes to their appearance without undoing anything along the way. Some people remove their watch or even a shoe. During the debrief, a GP made a comment that stuck with me: “I was so focused on removing things that I completely forgot I could have been adding the entire time”.

This is exactly the position the UK finds itself in, continuing to follow self-imposed constraints while the very capabilities needed to build something meaningful are right there in its grasp. The failure to think differently has resulted in millions of its people ensnared in a cost-of-living crisis, including 4.3 million children growing up in poverty.

But the real negligence is that chronic underinvestment actively shrinks future productive capacity. The UK is not just failing to mobilise idle resources to meet pressing needs today; it’s ensuring that it will be even less capable of delivering prosperity tomorrow.

Beyond the immediate human cost of inaction, the UK faces impending domestic challenges that demand the very fiscal response that the current paradigm prevents. AI disruption, an ageing population and the ongoing climate transition all require public investment over long time horizons that don’t fit neatly into annual budget cycles. The inability to meet these challenges not only undermines the UK’s global economic influence but risks the future of democratic governance itself.

More than ever, the UK needs brave leadership to chart a new course. Keir Starmer clearly recognised this in his Plan for Change speech when he invoked President Kennedy’s famous moonshot: “We choose to go to the moon in this decade and do the other things, not because they are easy, but because they are hard”. Kennedy’s words weren’t just rhetoric — they were a radical departure from the fiscal restraint that had preceded them, made at a moment when the US was quickly ceding ground to the Soviet Union. The technological dominance that the US economy enjoys today can be directly traced back to the decades of strategic public investment that began with Kennedy’s courage to defy convention. Starmer may have chosen the easy path but that doesn’t have to define Britain’s future.

Naturally, sceptics will point to the bond market as the reason for why the UK can’t engage in the fiscal expansion that is needed. But as Cambridge economist Dimitri Zenghelis notes, “What unsettles the bond market is not the level of UK public debt… It is doubt about the UK’s ability to grow without requiring persistently high interest rates.” This is the doom loop in action. Decades of underinvestment have left the UK struggling to grow without triggering inflation – not because demand is too high, but because productive capacity is too low. The solution isn’t paying down the debt, but bold investment in productive capacity that breaks the cycle.

Reeves’s £120bn infrastructure investment and scrapping the two child benefit cap are steps in the right direction but her debt reduction targets constrain the economy far below what is needed. As a monetary sovereign free from solvency risk, the UK should set fiscal targets based not on abstract debt ratios but on real economic outcomes: increasing investment as a share of GDP, closing the infrastructure gap, reducing economic inactivity or lifting millions out of poverty. This means building transport links in underinvested regions, expanding childcare so parents can work, retraining workers in high-demand skills, modernising the energy grid and constructing affordable homes. This isn’t reckless borrowing; it’s investing in what matters.

Years of austerity have conditioned the UK to accept artificial constraints as if they were immutable economic laws. But like a horse with a rope around its neck that’s no longer tied to its post – the UK is constrained only by the belief that it cannot move. The resources are there. The needs are urgent. All it needs to do is go.